There are many websites that discuss the three CPF Minimum Sum Schemes which determines how much CPF Life payout you can look forward to after 65 years old. CPF Life is our national annuity scheme for retirement and CPF Board itself has a whole repertoire of explainers and videos on the topic.

Still, with the multitudes of decisions and objectives involved, it can get daunting and confusing after a while. What this article hopes to achieve is to summarize the gist of what you need to know, especially for those who are less than 10 years away from the age of 55 which is when you should start to get more serious.

Before we go further, a lowdown on what happens from age 55 to 65 which you need to know:

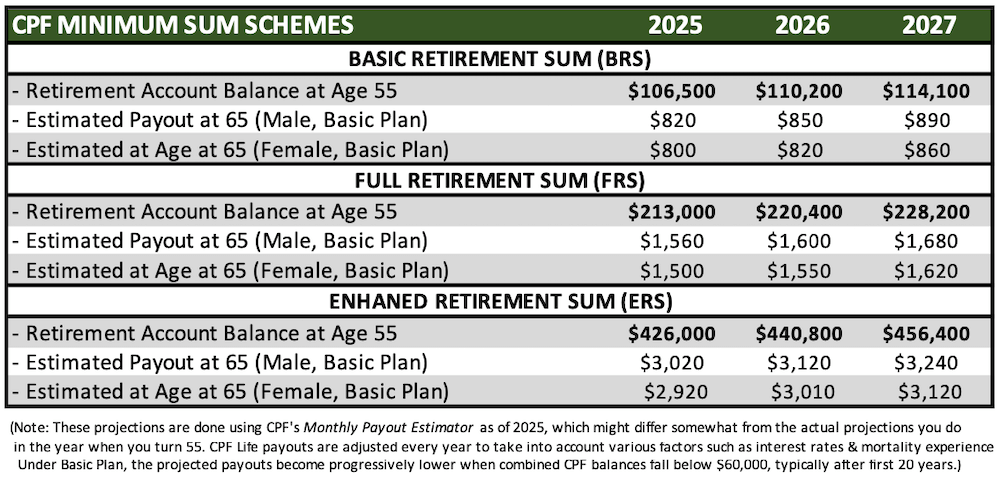

- At 55, everyone is allowed to withdraw a minimum of $5,000 if you so wish, after which your Special Account (SA) funds (which will be closed after that) first, followed by Ordinary Account (OA) funds, will be swept to a newly-minted Retirement Account (RA), up to the FRS amount of $205,800 in 2024. This FRS amount goes up annually at about 3.5% (see table below)

- For those who do not have sufficient funds in SA and OA combined to meet FRS, you can pledge your property in which case CPF will sweep only up to the BRS amount (half of FRS) at 55 to your RA.

- The funds in your RA will earn the same interest as what you used to earn in SA but these will be stashed away and are “untouchable” for the next 10 years until it is paid as a lumpsum premium to join CPF Life at 65, which is when your payout starts

- To get higher payouts, you are allowed to top up above the FRS amount, up to the maximum of ERS set for that year, using OA funds or even cash, anytime from 55 to 65 before the payout starts.

- The FRS is set at 2x of BRS, and ERS has been revised up from 3x to 4x of BRS starting from 2025.

- You will have to choose one of the three payout plans (Escalating, Standard or Basic) nearer to 65 or 70 before your payout commences

Understand there are three decisions you need to make with regards to CPF Life:

1. Do you want to start the payout at age 65 or 70?

Delayed gratification will translate into a higher payout. However, we kind of suspect the large majority of people are going to opt for 65, so that’s going to be our assumption for the rest of this article and which forms the easy answer to this question.

2. Which of the three payout plans would you go for?

There are three payout plans which CPF Life offers (see diagram below) with the default being the Standard Plan. Which plan you select affects not just how much is the projected payout you will receive, but how much of your Retirement Account (RA) balance will go into annuity premiums at 65, thus affecting the bequest or how much your beneficiary will receive upon early demise. There’s an excellent video on this topic posted on our home page.

Both the Escalating and Standard Plan require that the whole balance (including interest earned) in your RA be invested into the common pool as annuity premium at 65, which means you will get back less in bequest. This is because you can’t get back the monies (as well as the interest earned) that go into the common pool of annuity premiums as that’s what funds the whole scheme when any CPF member’s funds are depleted. For this reason, even though Standard Plan gives the highest payout amount from the start at 65, we will assume most people will opt for the middle-ground option of the Basic Plan in this article, where only 10-20% of your RA balance will be used for annuity premium.

3. How much money do you want to top up into your RA

The last decision is the hardest and requires the most parsing and preparation. It will be hard to discuss this question without any numbers. To exemplify, we will look at a male who turns 55 this year who opted for the Basic Plan. You can easily pluck the numbers for the Standard or Escalating plan from Monthly Payout Estimator on CPF website (Note: For those below 55 years old, you need to fiddle around until you get to the part where it bypasses Singpass login somehow, and enter your year of birth as if you are 55 years old this year)

The discussion for topping up to RA is more relevant for those with excess funds in OA, this pertains more to the middle-class. As CPF statistics on its website does not breakdown in terms of income, it’s hard to deduce this but we will assume the average middle-income salaried worker would have accumulated with compounding interest approximately $600,000 in his OA and $300,000 in his SA over a 30-year career until 55. We would also assume that by age 55, he would still owe about $200,000 in amount withdrawn for housing after making progressive return of monies to CPF over time. This means at 55, he would have $400,000 sitting in his OA earning him risk-free return of 2.5% p.a.

We will run the numbers for someone who turn 55 in 2025 for this discussion. At 55, SA funds will be swept to the newly-minted RA, up to the mandated FRS limit of $213,000, which then leaves a balance of $87,000 to be returned to OA after which SA will be closed. Though FRS gets adjusted up by 3.5% inflation every year, the compounding higher interest of SA (before 55) will take care of that to ensure there’s always more than enough to get swept up to the FRS for a middle-income earner.

However, with FRS, the projected payout for a Basic Plan will start at $1,560 in 10 years. You can easily double this payout to $3,020 by topping up with another FRS equivalent sum of $213,000 so that your total RA balance starts off at $426,000 in 2025, using a combination of OA balance or cash. You can do this in one lump sum or progressively over the next 10 years before the payout starts. It can be any amount but it’s capped at the ERS for that year.

In fact, you can get even higher payout than what’s shown in th table above, by progressively topping up each year an additional 3.5% of the ERS amount as it gets adjusted up. This is because when it comes to topping up to the ERS limit, CPF will not factor in the rise in RA balance due to the interest earned in the past year (unlike when transferring OA funds to SA to earn higher interest before 55). Going by our estimate, that’s another $174,000 of top-ups which would likely push your payout close to or surpassing $4,000 by 65 (caveat: this number might differ as topping up $174,000 in lump sum just before 65 or incrementally 3.5% of ERS per year, will yield different estimates from had you been able to top up fully at 55)

The question – Is that a wise move? It’s a difficult question to answer as you don’t know how long you will live. There’s an inherent conflict between the objective of investment or maximising gain, versus that of hedging longevity risk, where the latter is what CPF Life is really meant for.

There’s also this period which most might overlook between the age of 55 to 65, which we like to refer to as “pre-retirement” years in this website, analogous to pre-school years for young ones. This is the period where many will likely go into some kind of reduced pay mode like semi-retiring or become a full-time care giver, whether intentionally or due to poor health. The financial strain as a consequence during this pre-retirement phase is often overlooked. You have to get past pre-retirement years to get to retirement!

To answer that question, let’s compare using two simple scenarios: First, he’s sticking with FRS limit with no additional top-up to RA in which case his final OA balance after 55 would be $487,000 with the balance SA funds $87,000 added. Second, he tops up using 100% OA funds to join CPF Life at the highest ERS limit of $426,000 at age 55 in 2025:

| OA Bal | From 55 | Age 55-64 | From 65 | Age 65-74 | Total Over 20 Yrs | ||

| OA Interest^ Per Month | Income Over 10 Yrs | CPF Life Per Month | Total* Per Month | Income Over 10 Yrs | |||

| FRS | $487,000 | $1,015 | $121,750 | $1,560 | $2,575 | $309,000 | $430,750 |

| ERS | $274,000 | $571 | $68,500 | $3,020 | $3,591 | $430,920 | $499,420 |

^ Based on 2.50% * OA interest plus CPF Life payout

It may seem that the best thing to do is to go for the highest tier of ERS with his spare OA funds of $487,000 after turning 55, after all there’s still $487,000 less $213,000 or $274,000 left in his OA to earn the risk-free return of 2.5%. If you just withdraw the OA interest earned at the end of every year, that still translates to an extra spending money $571 during the first 10 years of your pre-retirement years from 55 to 64. Yet, you can increase your total income from age 65 almost by a thousand dollars from $2,575 to $3,591!

If we suppose he lives till 75 years old and look over a period of 20-year, that difference is about $70,000, or 16% more, in terms of total income you received from both CPF OA interest and CPF Life payout combined. However, the trade-off here he would cut his income by 40% during your pre-retirement years from age 55 to 64, where a $1 today is worth more than the same dollar 10 years later. And the utility value of that extra income during the pre-retirement years is probably also worth more when he still has the energy and mobility to enjoy life?

Of course, the difference will be significant if you live another 20 years until 95 (Singaporean’s average life span is 80 to 85 years old depending on gender). This purpose of this article is not to make the case for or against topping up to the maximum of ERS limit at 55. Rather it is to set you thinking early and making financial preparations for this third decision you have to make regarding CPF Life as there are many other moving parts and other factors to consider for example:

- What are your goals and financial needs during pre-retirements years vis-à-vis actual retirement?

- Would you still have other income sources to cater to needs arising during this pre-retirement period?

- Would you be able to generate steady return of 2.50% or even higher using your cash reserves? If yes, you have less need to rely on CPF OA for income during pre-retirement which warrants deploying that for maximum CPF Life payout

In fact for the last decision, to take it to the extreme, you even may want to deploy maximum OA funds or even cash to maximize CPF payout to almost $4,000 monthly after 65, by topping up annually another 3.5% of increased ERS limit from age 55 to 64. With the highest income after 65 assured, it leaves you with a greater peace of mind to simply drawdown more on your OA beyond just the interest earned and thus the balance during pre-retirements where you possibly get the most bang for your buck! YOLO.

There’s no easy answer, and there’s no right or wrong. After all, it’s your hard-earned money after working for a lifetime.

This blog seeks to improve financial literacy amongst Singaporeans and provide the “best-in-class” knowledge for financial planning to help achieve the best retirement plan. We also hope to become the conduit to channel funds from the well-to-do in this country to the poor and weak as part of our social mission.

| ACTIONABLE STEPS: (This article is especially pertinent for those in the 45-55 age group who are less than 10 years away from the CPF withdrawal age of 55) 1. Browse through CPF website for the latest schemes and guidelines on CPF Minimum Sum schemes and CPF Life 2. Mull over each of the three decisions you got to make pertaining to CPF Life and how much payout you will like to receive after 65 3. Watch the video that explains how the different CPF Life payout plans and the considerations with the link on our home page 4. Consider a more balanced viewpoint for your financial and retirement needs in both the pre-retirement and the actual retirement phase. |

Disclaimer: Neither PropertyWise Pte Ltd, the operator for this website, nor any of its editorial team writers or external contributors are in the business of providing financial advice. We are not licensed or regulated by MAS under the Financial Advisory Act (FAA) in Singapore. All information presented are opinions of the writers and any representations given, whether by way of example, illustration or otherwise, are purely portfolio allocation advice and not recommendations or inducements to buy, sell or hold any particular investment product or class of investment product. All opinions are generic in nature and are not tailored to the particular circumstances of any reader. Seek advice from a qualified financial advisor before making any investment decision.

Though every effort has been made to ensure the accuracy of the information and figures presented, we make no representations or warranties with respect to the accuracy or completeness of the contents in this blog and specifically disclaim any implied warranties or fitness for a particular purpose. You are advised to validate the information especially content related to CPF retirement account and CPF Life.

We shall not be held responsible for any financial loss or any other damages suffered whatsoever, directly or indirectly, if you choose to follow any of the advice or recommendations given in this blog.