Term insurance policies are designed to provide substantial coverage at a fraction of the cost of whole life insurance. This makes it an affordable option for individuals seeking high coverage to protect their family’s financial future without breaking the bank, and most crucially, when they most needed that protection – young kids and aging parents.

Before I talk about Great Eastern (GE)’s plan, let’s first revisit the case for term insurance.

Why Term?

Indeed, there is a common misconception that term insurance is a waste of money if no claim is made. However, understanding the true value of term insurance can help dispel this myth. Here are some key reasons why term insurance can be such a valuable investment:

- Term insurance provides a large death benefit that can cover major expenses, including mortgage payments, educational costs for children, and daily living expenses. This ensures that your loved ones can maintain their standard of living even in your absence.

- If you have significant debts, such as a home mortgage or personal loans, term insurance ensures that these liabilities are not passed on to your family. The policy payout can be used to settle debts, relieving your dependents of financial stress.

- Majority of term insurance policies, including GE’s Great Term, offer the option to convert to a whole life or endowment policy without evidence of insurability. This means you can purchase a large amount of insurance protection while you are young and healthy and, should you decide to convert to a whole life or endowment policy with cash value later, you have the flexibility to do so even if you are no longer eligible for new insurance protection at that time. This feature provides additional peace of mind, knowing that you have that option to secure lifetime coverage and build cash value without undergoing further medical examinations or underwriting processes.

What Should You Consider in Term Insurance?

Cost, or affordability, is without doubt the primary reason for buying term, which in turn is largely determined by the amount and length of coverage.

As a financial services consultant, it is crucial to have an in-depth understanding of a client’s overall financial situation and objectives before making any recommendations. Still, in so far as one can afford the premiums, the general advice would be to go for a higher coverage as well as a longer coverage until 100 years old.

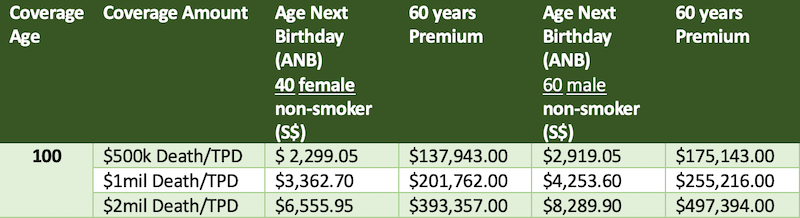

To illustrate why so, let me use the table below which shows the premiums payable for someone who is 40 years old today, both female and male, non-smoker, who buys three different coverage levels of term insurance of $500,000, $1 million and $2 million, until the grand age of 100 years old:

1. Why You Go For Minimum of $1 Million Coverage?

Higher Cost Ratio

As you can see from the table of premiums, if you should live right until the end of 100 years old, total premiums paid for a $2 million coverage is just 20% and 25% of the payout respectively for a female and male. However this total sunk costs as a percentage of payout rises to 28% and 35% when you opt for a $500,000 coverage.

For the middle-ground option of $1 million coverage, the cost ratio works out to be 20% and 26% respectively, not very different from $2 million coverage

Inflation

Over long periods like 40-60 years, inflation significantly erodes the purchasing power. While $1 million might seem substantial today, its real value will decrease over time. Setting a high coverage amount helps mitigate the impact of inflation, ensuring the utility value of the payout remains somewhat the same.

Provide Adequately for Dependents

Inflation hits hard on those with aging parents and young children especially with the acute rise in costs for healthcare and education in Singapore. Adequate coverage ensures that dependents can be better taken care of should they lose the breadwinner in the family.

Rising Mortgages

Property prices in Singapore are amongst the highest globally. Rising prices also lead to a much higher level of mortgage debt over time. Having a substantial term insurance coverage helps ensure that your dependents can manage the mortgage and retain the family home in case of your untimely demise.

2. Why Should You Cover Until Age 100?

Certainty of Death

Life insurance is a guaranteed benefit as everyone eventually passes away. Likewise, with the average lifespan of Singaporeans at 80-85 years old, opting for coverage until age 100 for a term insurance dictates that the policy will pay out eventually to your beneficiary when the untoward happens.

Proper Planning For Premiums Payment Post-Retirement

While concern regarding the affordability of premiums post-retirement is a valid one, this could be planned for and set aside early through investments or savings accumulated during your working years. When premiums cause too much of a financial strain after retirement, one could even consider transferring the policy to your children which is the next point.

Transferring of Policy to Children

By passing the responsibility of premium payments to your children after retirement, the policy remains active with a substantial payout which becomes a form of meaningful inheritance for your loved ones.

For instance, consider the case where you service the premiums for a good half of the 60-year premium term and transfer the policy to your children at age 70, they might not necessarily service the premiums for as long as you did, yet that eventual $1 million payout can significantly aid them and their next generation considering how we are facing a cost-of-living crisis in the years ahead.

Great Eastern: Your Trusted Partner for Term Insurance

Finally, let’s talk about GE’s Great Term Insurance and why it could be one of your top picking:

1. Affordability

Great Term insurance is one of the most competitive term insurance plans in the market which you can validate easily at CompareFirst.sg. For all the reasons spelt out earlier, that’s how we ensure you can secure significant financial protection for their families without straining your budget.

2. Extensive TPD Coverage

For most insurers, Total Permanent Disability (TPD) coverage provides financial support in the event of a severe and lasting disability that occurs before the age of 65 years old which is typically defined as a permanent state of incapacity to perform any work, occupation, or profession to earn or obtain any wage, remuneration, or profit at any time during and thereafter, OR presumptive TPD (loss of use) evident by:

- Loss of sight in both eyes

- Loss of use of two limbs at or above the wrist or ankle

- Loss of sight in one eye and loss of use of one limb at or above the wrist or ankle

Great Term insurance offers extensive coverage for presumptive TPD (loss of use) even after the age of 65, applicable for the entire policy term, up to age 100.

3. Value of a Financial Service Consultant

In the realm of insurance, an agent’s value lies in his or her ability to provide great insights which help customers better understand the importance and type of coverage, whether for themselves or their loved ones. This understanding is crucial for effective legacy planning.

By comprehensively detailing all the benefits and provisions of GE’s Great Term insurance as well as the case for why term insurance, clients can make better informed decisions to secure their families’ financial future.

| ACTIONABLE STEPS: 1. Review your need for a higher insurance coverage 2. Compare premiums at the national comparison site CompareFirst.sg 3. Get one of the most competitive quote for term insurance by Great Eastern by reaching out to the writer (details below) |

Disclaimer from Financial Representative: Any views, opinions, references, assertions of fact and/or other statements that a financial representative may set out on his/her social media account(s) or otherwise are his/her personal views and are not necessarily the views held by the Great Eastern group. The Great Eastern group disclaims any liability whatsoever that may arise out of or in connection with such statements.

Disclaimer from MortgageFree6Years: Neither PropertyWise Pte Ltd, the operator for this website, nor any of its editorial team writers or external contributors are in the business of providing financial advice. We are not licensed or regulated by MAS under the Financial Advisory Act (FAA) in Singapore. All information presented are opinions of the writers and any representations given, whether by way of example, illustration or otherwise, are purely portfolio allocation advice and not recommendations or inducements to buy, sell or hold any particular investment product or class of investment product. All opinions are generic in nature and are not tailored to the particular circumstances of any reader. Seek advice from a qualified financial advisor before making any investment decision.

Though every effort has been made to ensure the accuracy of the information and figures presented, we make no representations or warranties with respect to the accuracy or completeness of the contents in this blog and specifically disclaim any implied warranties or fitness for a particular purpose. You are advised to validate the information especially content related to CPF retirement account and CPF Life.

We shall not be held responsible for any financial loss or any other damages suffered whatsoever, directly or indirectly, if you choose to follow any of the advice or recommendations given in this blog.