Many financial advisors like to say that relying on CPF Life payouts when we turn 65 years old is not enough to meet our retirement needs. Just how true is that?

To answer that, let’s break this into two sub-questions and we will delve into it one by one.

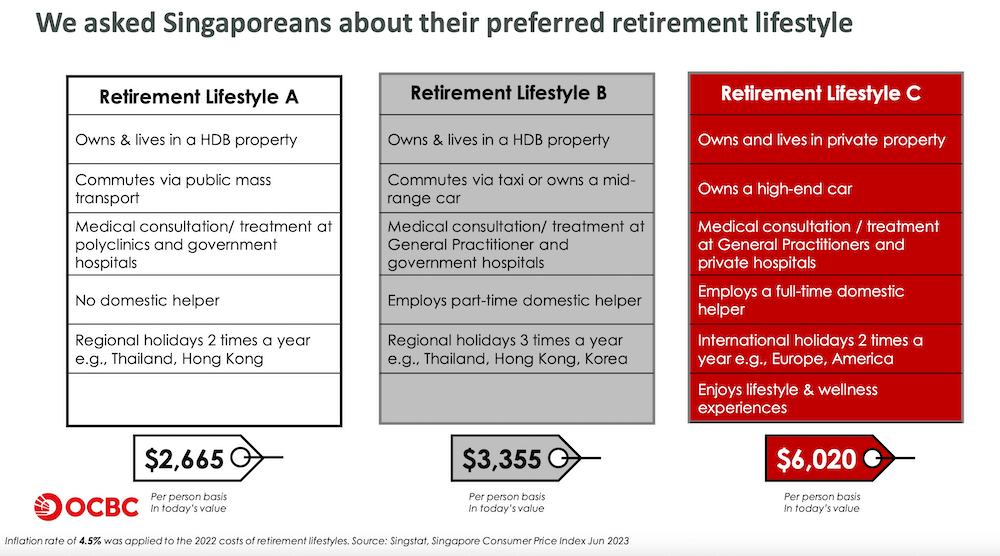

1. How Much Is Needed to Retire in Singapore?

Adequacy is a matter of subjective judgement or preference. So, the answer to the question of how much is too much or too little is best based on some research findings. In the latest annual OCBC Financial Wellness Index survey, which has become a generally-accepted benchmark, done in 2023, the cost of living has been broken down into three retirement lifestyles:

The most important words in the whole slide above is the phrase “in today’s value” appearing below the costs shown. These costs were derived from its previous year 2022’s costs with an assumed 4.5% inflation. Now, what will this number look like if we just assume a 20-year horizon with an average inflation of 3.5%?

Lifestyle A $5,303

Lifestyle B $6,676

Lifestyle C $11,979

We use a 20-year period as not everyone reading this article will start planning at age 35. Most likely, you will be in your mid-40s, when you start thinking more seriously about retirement planning which got you here. If I just use Lifestyle B as a middle-ground option, you are staring at a cost of living at almost $7,000 in nominal value when you hit 65 years old! The problem is, I suspect, most of us aspire to live better like a Lifestyle C, especially after slogging away a whole lifetime to deserve it.

There you have it, based on our estimates, it’s about double of what a survey research would tell us which we put as $5,000, $7,000 and $12,000 respectively for Lifestyle A, B and C.

2. How Much Can I Get from CPF Life?

Now let’s look at how much can we get from CPF Life, factoring in the recent changes announced where the Enhanced Retirement Sum (ERS) amount will be raised to be 4x that of the Basic Retirement Sum (BRS) starting from 2025.

We have a whole article dedicated to “CPF Life – The 3 Decisions You Need to Make” which you should read. For our purpose here which is to try and get the highest payout possible, and to keep it short, we will assume most people will opt to start receiving their payout from the earliest age of 65, and would also opt for the Standard Plan.

(Note the Standard plan is the default plan selected for you by CPF. Though it has the highest payout, you will get back less in request as all of the RA balance plus interest would be vested into the common pool as annuity premium. There’s an excellent video explainer on this which we provided the link in our home page.)

To determine what’s the maximum you could get from CPF Life, we will look at the situation for a male who turns 55 in 2025 as that’s the first year for the latest change in ERS limits going up to four times of BRS. You can always go to CPF Life Estimator on CPF website to fiddle with the numbers for your own situation.

The table above shows the change in ERS limits (from 2025) highlighted in yellow for those turning 55 in the respective years, as well as the projected payout from age 65 based on both the Basic and the Standard Plan. For the latter, you are looking at a monthly payout of $3,310 from age 65 for a male who turns 55 in 2025 and who has excess Ordinary Account (OA) balance of $213,000 to top up to his Retirement Account (RA) at 55. This is after CPF first sweeps $213,000 from your Special Account (SA) to fulfil the FRS limit of $213,000. In total, you would have set aside a total of $426,000 in RA at age 55 in 2025 to join for CPF Life 10 years later.

Clearly, even at the highest tier of ERS payout of $3,310, you are still unable to cover retirement Lifestyle A, let alone the more sought after Lifestyle B & C. Supposed the average middle-class worker will settle for a retirement lifestyle somewhere between that of B & C. This means you will still need around $10,000 per person in 20 years’ time. With risen life expectancy (which may come with higher medical costs), it’s not inconceivable to live till 84 to 85 years. For a couple who live from 65 to 84, that’s about 20 years x $10,000 per month x 2 persons which means you will need at least $4.8 million worth of retirement assets to last you the distance. That conventional idea of simply “killing the goose” by selling away a private property and downgrading to a HDB to fund our retirement may need some re-examination.

This underscores the urgent need for proper retirement planning today.

This blog seeks to improve financial literacy amongst Singaporeans and provide the “best-in-class” knowledge for financial planning to help achieve the best retirement plan. We also hope to become the conduit to channel funds from the well-to-do in this country to the poor and weak as part of our social mission.

| ACTIONABLE STEPS AFTER READING: 1. Go through the retirement lifestyle A, B & C in the OCBC survey, and do a more personal projection based on the idiosyncratic needs of your own retirement after 65, when all your mortgages and debts are cleared. Remember to assume an inflation rate of 3.50% per annum to arrive at the figure after 20 years 2. You may access OCBC Financial Wellness Index for more in-depth understanding 3. Do some serious retirement planning today and start speaking to your financial advisor or find out more and improve your financial literary through online resource like this website and others. |

Disclaimer: Neither PropertyWise Pte Ltd, the operator for this website, nor any of its editorial team writers or external contributors are in the business of providing financial advice. We are not licensed or regulated by MAS under the Financial Advisory Act (FAA) in Singapore. All information presented are opinions of the writers and any representations given, whether by way of example, illustration or otherwise, are purely portfolio allocation advice and not recommendations or inducements to buy, sell or hold any particular investment product or class of investment product. All opinions are generic in nature and are not tailored to the particular circumstances of any reader. Seek advice from a qualified financial advisor before making any investment decision.

Though every effort has been made to ensure the accuracy of the information and figures presented, we make no representations or warranties with respect to the accuracy or completeness of the contents in this blog and specifically disclaim any implied warranties or fitness for a particular purpose. You are advised to validate the information especially content related to CPF retirement account and CPF Life.

We shall not be held responsible for any financial loss or any other damages suffered whatsoever, directly or indirectly, if you choose to follow any of the advice or recommendations given in this blog.