We have all heard of CPF Life, the national annuity scheme, but think of that of something to research and find out only when we are near to 55 years old which is when our CPF funds get swept to a new CPF RA (Retirement Account) to be set aside for CPF Life scheme. Do you know that there’s a way you can benefit immediately from CPF Life?

Most of us give some kind of monthly allowance for our aging parents above the age of 65, especially if they have stopped working. Let’s assume this amount averages around $1,000 a month, which we give in cash. Do you know there’s a simple way you can give them this amount indirectly via CPF Life which has three immediate benefits?

The simple idea works like this: Get a loan to top up their RA, so they get $1,000 more monthly payout from their CPF Life immediately (for those above age 65)! The best way to do this is to borrow from your existing property in the form of a mortgage equity withdrawal loan (MWL), or what is commonly known as home equity term in our industry. Or simply term loan in short. You still “give” to your parent but indirectly, by servicing a higher monthly repayment.

Before I go further, unfortunately MWL is only allowed for private properties, so this idea will not work completely on HDB properties. First, what is MWL? If you have been diligently paying down on your private property loan for some time, you would have reduced the principal sum outstanding quite substantially, whilst the property valuation has also risen. This means you can now take out more loan secured against the same property as the equity portion (as opposed to debt) of the valuation has increased, hence the name equity withdrawal loan. You are “withdrawing” from this increased equity over time.

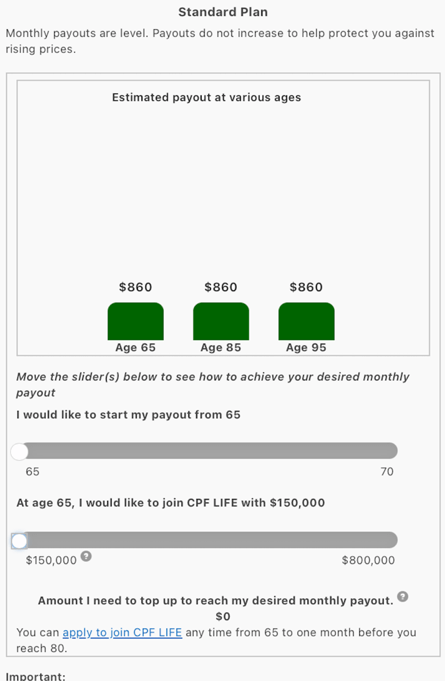

How does this benefit you? Let us use a fictitious example to illustrate. Suppose John currently services a mortgage of $800,000 at 3.25% on his residence property with 20 years tenure remaining. He gives his dad about $800 allowance every month. His father, born in 1959, will turn 65 in 2024 which is when he will start receiving his payout from CPF Life estimated to be $860 on the standard plan based on his current RA balance of $150,000. You can estimate the amount of payout using the CPF Life Estimator on CPF’s website.

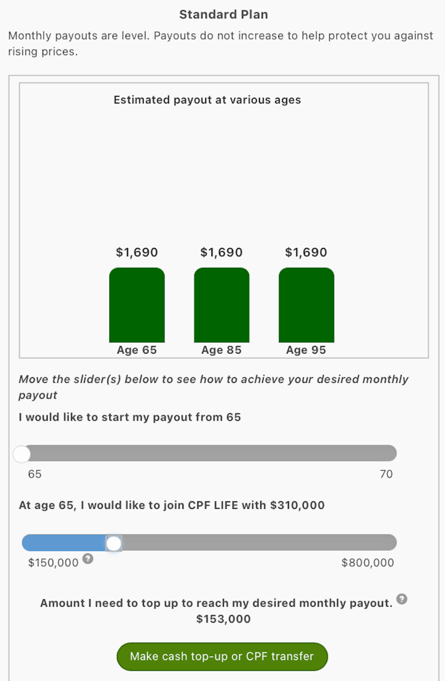

Can you increase this CPF Life payout and is there a cap? The answer is yes. John can top up his dad’s RA with cash up to the ERS (Enhanced Retirement Sum) for that year, which is set at $308,700 (for the year 2024). This limit will go up to 4x of BRS (Basic Retirement Sum) at $426,000 from 2025. The table below shows the minimum sums which are published by the Board for the 5-year period 2023 to 2027. For your information, those turning age 55 during this period will automatically get their CPF funds swept from first their SA followed by OA to their newly-minted RA, up to the FRS (Full Retirement Sum) amount for that year. You can read more on that in this related CPF Life article.

Using the CPF Life Estimator, John determines that by topping up his dad’s RA with a lump sum cash of about $153,000 (hence nearing the cap of $308,700 in 2024), he could increase his dad’s projected payout from $860 to $1,690, an increase of about $830.

John decides to cleverly make use of MWL on his existing mortgage by gearing up from $800,000 to $953,000 and cashing out a lump sum of $153,000 for this purpose. He’s able to do so as he has used little CPF towards the property and this is his only mortgage in Singapore (there are regulatory guidelines on how much you can encash on MWL). Let’s take a look at what’s the impact on this monthly cashflow in terms of mortgage repayment.

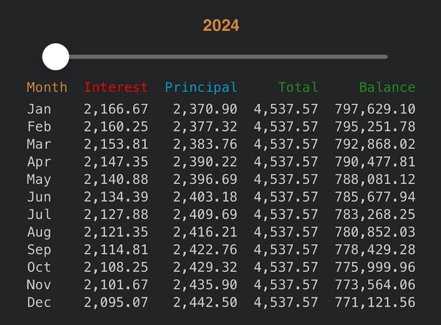

Outstanding loan = $800,000

Interest rate = 3.25%

Tenure = 20 years

Monthly Repayment = $4,538

1st Monthly Interest = $2,167 (48%)

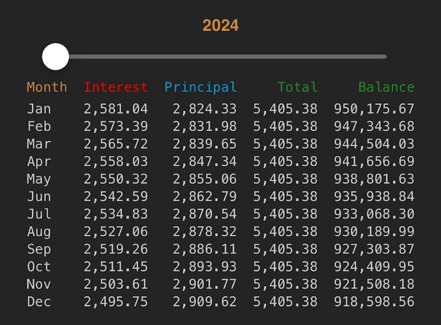

Outstanding loan = $953,000

Interest rate = 3.25%

Tenure = 20 years

Monthly Repayment = $5,405

1st Month Interest = $2,581 (48%)

Using just the first year’s amortization in 2024 to illustrate, even though John’s monthly repayment goes up by $867 from $4,538 to $5,405, it still makes a lot of financial sense to do this and I will give you three perspective why so.

1. Cash Flow Perspective

Instead of giving his dad $800 allowance every month, John pays the bank a higher monthly repayment by $867. Beginning on his 65th birthday in 2024 this year, his dad now gets more or less the same additional $830 from CPF Life instead of from his son. In short, there’s no material impact on John’s cash flow every month, even at today’s high interest rate of 3.25% which will not stay high forever.

Of course, this only works if one of your parents is above the age of 65 where CPF Life starts for most (retirees also have the option to defer the start to age 70 for a higher payout).

2. Cost Perspective

What’s interesting is this: Even though there’s no change in John’s monthly cash flow, there’s real savings for John now. Not everything he pays is a “sunk cost” unlike giving his dad the $900 allowance previously. You can see the interest component is about half at 48% in the first month and this is set to go down over time with amortization. This means his real cost is only about half of $867 or around $430. His dad still gets the same increased amount of $830 from CPF Life payout, but John saves half that sum as he’s “paying himself” in terms of reducing the loan. Eventually he gets back this principal sum when he finally sells the property.

3. Benefit Perspective

There’s yet one more benefit to the whole set up. CPF Life payout is for life. His dad will continue to receive the payout totalling $1,690 even after John finished paying off his entire loan in 20 years. It does not matter if John should change his plans later and sell and upgrade his condo to a landed property, the lump sum of $153,000 borrowed will still get factored in his new purchase calculus and he will always service an interest component on it that’s much lesser than giving the whole allowance directly to his dad.

Eventually John will finish paying off the loan, but CPF Life payout continues. He also gets back any “unused portion” of the cash value built up upon the demise of his dad, albeit that will follow the allocation as per his dad’s CPF nomination.

You might have a concern what if the property market turns soft and the value of your property comes down leading to a negative equity (property valuation going below the outstanding loan) predicament? That may be a valid concern since you are increasing the loan-to-value, but the fact that there’s stringent guidelines in place that govern how much MWL one could encash means the bank has deemed your debt level to be comfortable before granting you the term loan. For example, for someone with a single mortgage, typically the total geared-up loan cannot be more than 70-75 per cent of the latest valuation minus the CPF used. In addition, your income must pass the tightened TDSR ratio of 55% before the bank will approve the new higher loan. The upshot is not everyone can avail themselves of MWL. So, when you do get it approved, there’s enough margin of safety built in to cater for the scenario of falling property prices.

In conclusion, more debt is not necessarily a bad thing if you know how to deploy it as good debt for either savings or investments. So, for those thinking of paying down your mortgage with your spare cash, think again. You may want to re-channel your funds for better use.

(The article was first published by Business Times on 18 Nov 2023)

This blog seeks to improve financial literacy amongst Singaporeans and provide the “best-in-class” knowledge for financial planning to help achieve the best retirement plan. We also hope to become the conduit to channel funds from the well-to-do in this country to the poor and weak as part of our socialmission.

| ACTIONABLE STEPS: (This idea works only for those giving monthly allowance for parents who are over the age of 65 where they could immediately draw down on the higher payouts) 1. Use the CPF Life Estimator to determine how much cash you will need to top up to your parent’s account 2. Explore with a mortgage broker or your existing bank how much you can still cash out on your existing mortgage 3. Run the numbers and see if it still make sense to re-juggle the cash flow in such a way as to make it into an increased annuity stream for your parents. |

Disclaimer: Neither PropertyWise Pte Ltd, the operator for this website, nor any of its editorial team writers or external contributors are in the business of providing financial advice. We are not licensed or regulated by MAS under the Financial Advisory Act (FAA) in Singapore. All information presented are opinions of the writers and any representations given, whether by way of example, illustration or otherwise, are purely portfolio allocation advice and not recommendations or inducements to buy, sell or hold any particular investment product or class of investment product. All opinions are generic in nature and are not tailored to the particular circumstances of any reader. Seek advice from a qualified financial advisor before making any investment decision.

Though every effort has been made to ensure the accuracy of the information and figures presented, we make no representations or warranties with respect to the accuracy or completeness of the contents in this blog and specifically disclaim any implied warranties or fitness for a particular purpose. You are advised to validate the information especially content related to CPF retirement account and CPF Life.

We shall not be held responsible for any financial loss or any other damages suffered whatsoever, directly or indirectly, if you choose to follow any of the advice or recommendations given in this blog.